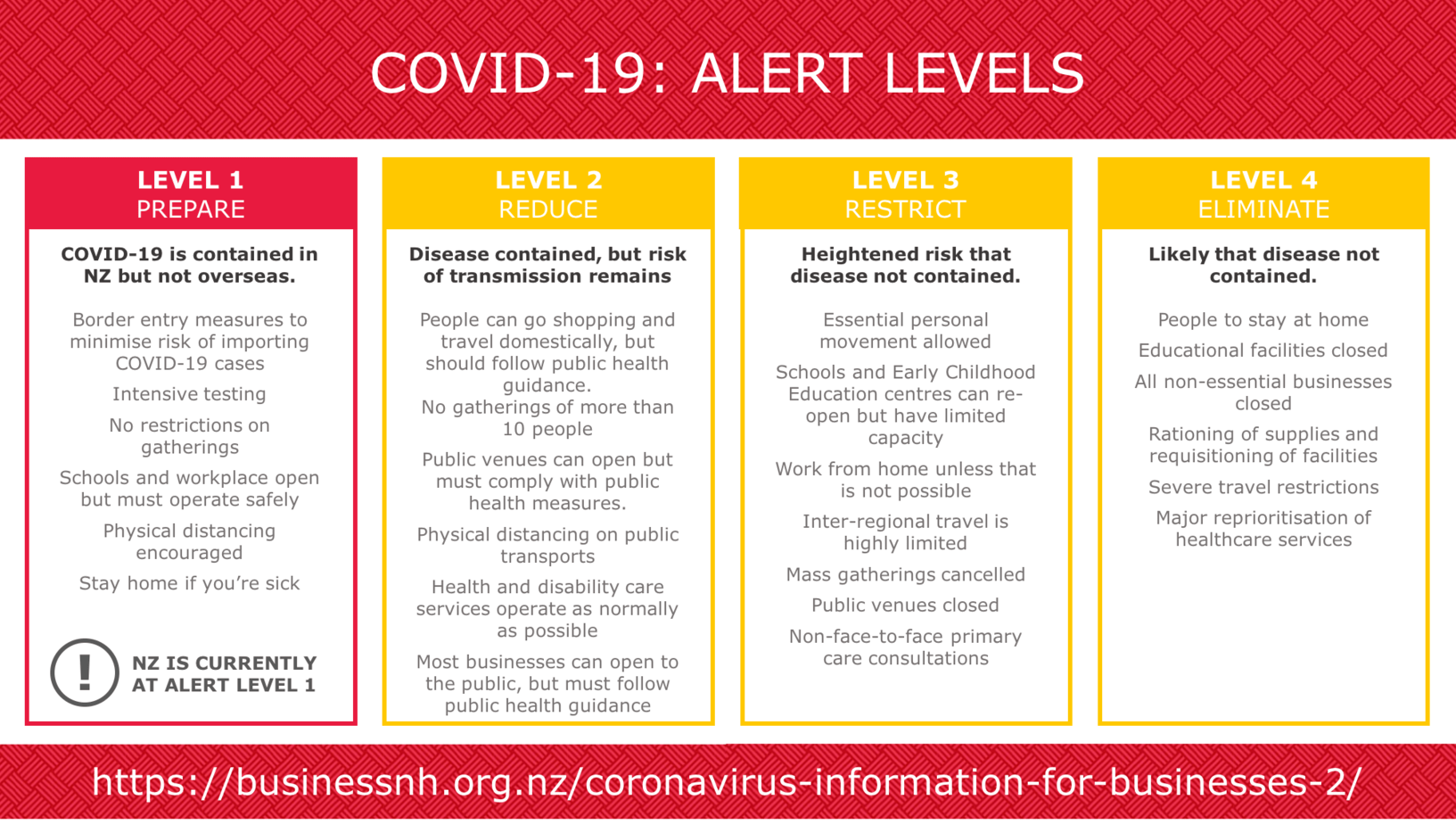

Latest COVID-19 News

Novel Coronavirus Map

Updated daily.

This webpage has everything you need to know about COVID-19 in one place. Find-out what help is available, get advice from industry experts and read the latest updates.

COVID-19 Videos

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

")

KEVIN O’LEARY – GENERAL MANAGER, BNH

Key discussion points:

- BNH support services

- Online resources

- Dealing with your landlord – Security checklist

- Who to call

- The business community spirit

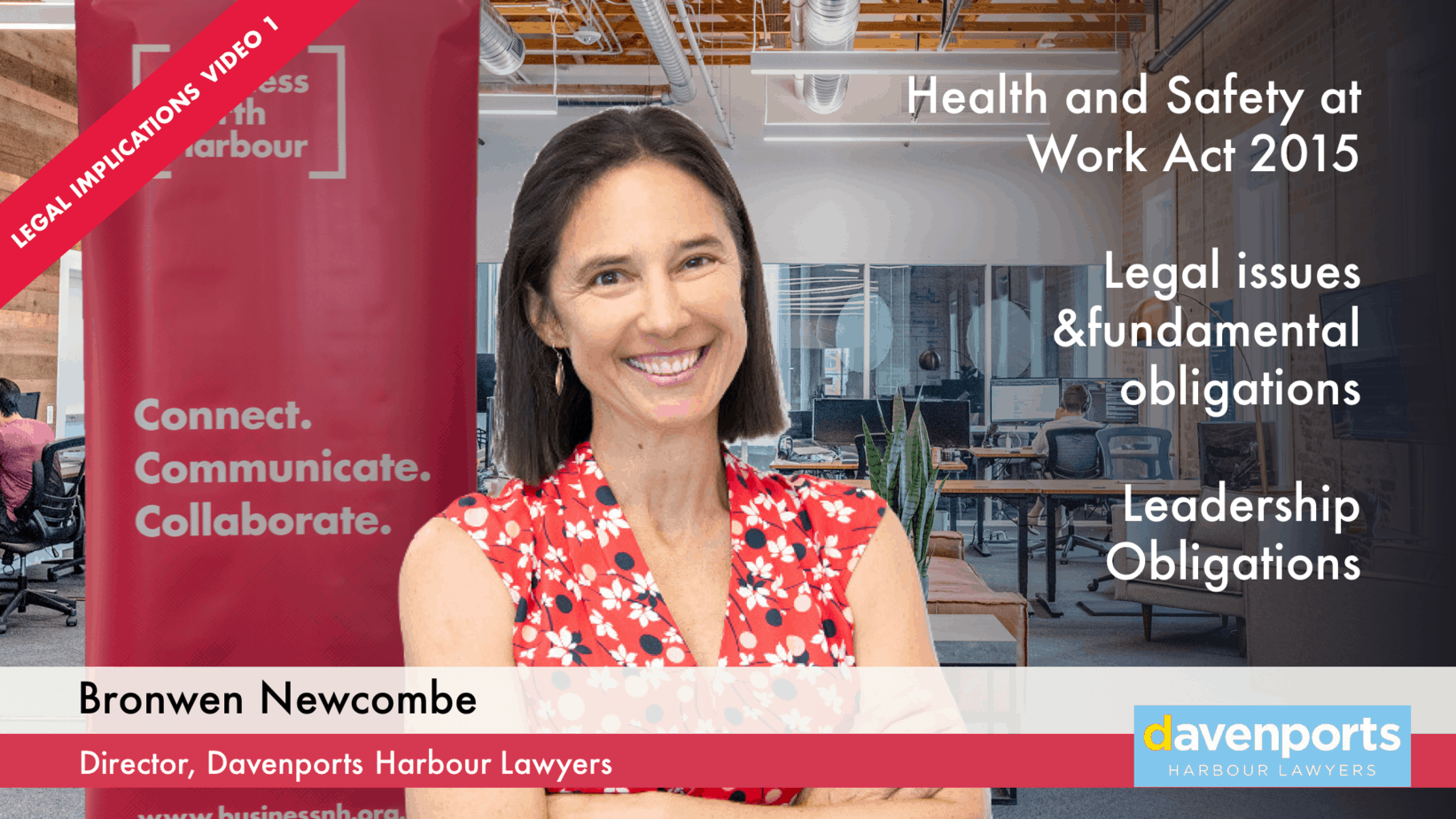

BRONWEN NEWCOMBE – DIRECTOR, DAVENPORTS HARBOUR LAWYERS

Key discussion points (video 1):

- Health and Safety at Work Act 2015

- Legal issues & fundamental obligations

- Employee COVID-19 Leave payments

- Online resources

- Employee COVID-19 Wage Subsidy payments

- Sole Traders

- Leadership obligations

Key discussion points (video 2):

- Redundancy

- Legal obligations & process

- Personal grievances

- EAP services

- Legal advice

SIAN JAQUET – EXECUTIVE COACH, PROFESSIONAL DIRECTOR AND KEYNOTE SPEAKER

Key discussion points:

- Mental resilience

- Managing anxiety

- Self-reflection

- Self-awareness

- Mental health

- Asking ‘are you OK?’

- Positive reinforcement

DAVID WILSON – GENERAL MANAGER, IT360

Key discussion points:

- Home office/remote working planning

- Placing your router

- Internet connections

- Cyber security

- Security assessment tool

- Online resources

GINA COOK – ADVISORY PARTNER AT BDO

Key discussion points:

- Government Wage Subsidy and other Government support options

- 30% decline in revenue rule

- Cash flow problems and loan repayments

- BDO resources to help businesses

- What to do if your suppliers are not paying you on time

- How to approach an accountant or a lawyer?

- What should you do if you don’t have the funds?

- What if your business strategy is not working?

- Reviewing business fundamentals

- Government financial support package for SMEs

BDO Article: COVID-19 Tax Response Act 2020

BDO Article: Wage Subsidy and Leave Payment FAQs

Business Tool: Government Wage Subsidy and Leave Payment Factsheet

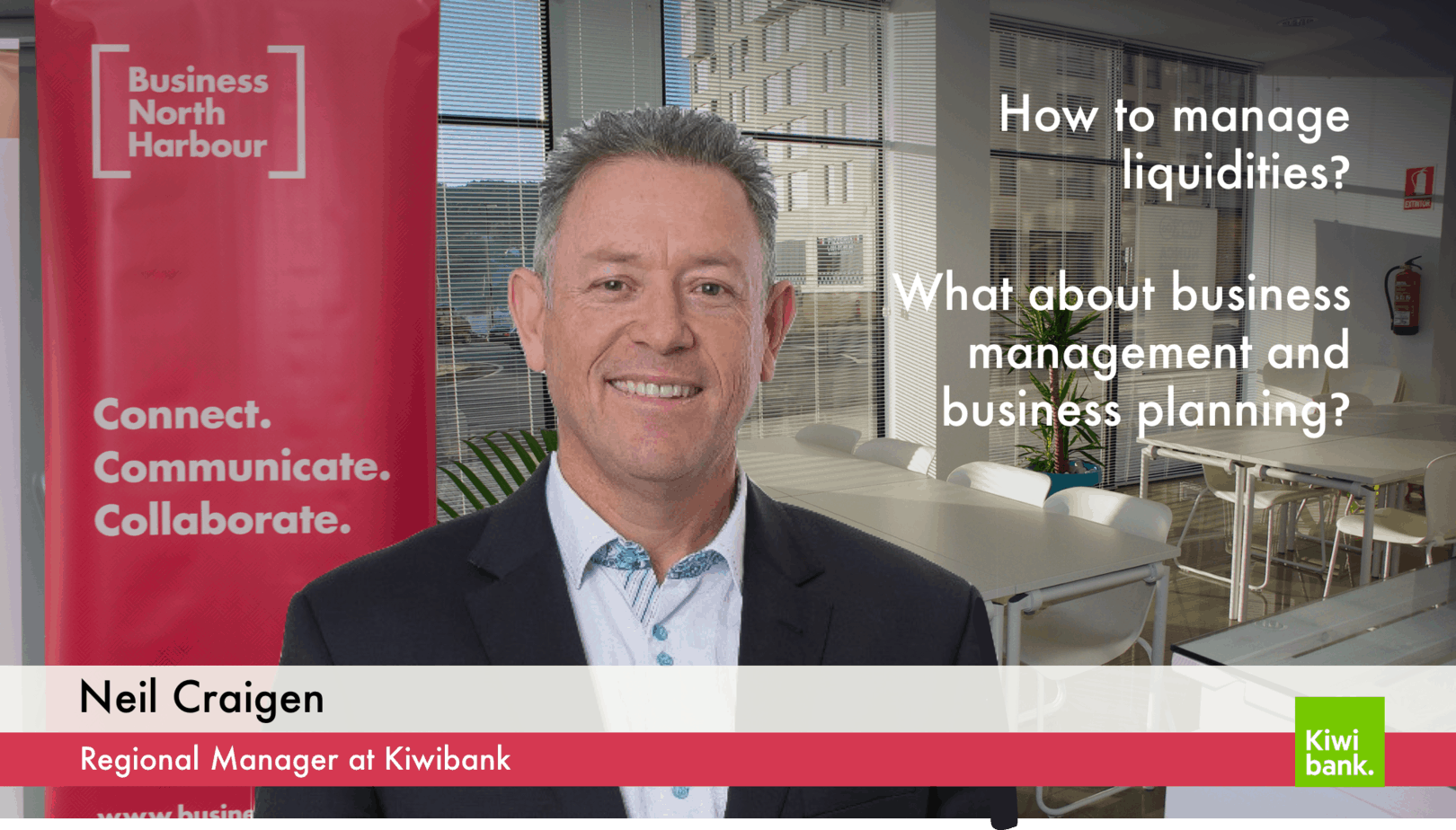

NEIL CRAIGEN – REGIONAL MANAGER AT KIWIBANK

Key discussion points:

- What can businesses expect if they want to communicate with their bank?

- Business Management and Business Planning

- How to manage liquidities

- Information about Business modelling

- BFGS (Business Finance Guarantee Scheme)

- Short-term credits to cushion financial distress

- Fundamental information business owners need to provide to benefit from their bank’s support

- Keep ourselves and our team safe

- Work/life balance when working remotely

Tax and Business Support Options

ECONOMIC RESPONSE PACKAGE

WAGE SUBSIDY SCHEME:

The COVID-19 wage subsidy scheme has been modified. This is to help businesses that need to shut down under Alert Level 4 pay workers for an extended period of time.

The modified wage subsidy scheme will support employers and their staff to maintain an employment connection and ensure an income for affected employees, even if the employee is unable to actually work any hours. Applications for the modified wage subsidy scheme will be open until New Zealand moves down from COVID-19 Alert Level 4. Applications can be made on the Work and Income website.

The wage subsidy scheme:

- supports employers adversely affected by COVID-19, so that they can continue to pay their employees;

- supports workers to ensure they continue to receive income, even if they are unable to work.

Use the Wage Subsidy Eligibility Tool.

BUSINESS CASH FLOW AND TAX MEASURES:

There are a number of business cash flow and tax measures that have been announced, including:

- Giving Inland Revenue the discretion to remit use-of-money interest (UOMI) for customers significantly adversely affected by COVID-19.

- Increasing the provisional tax threshold from $2,500 to $5,000 from 2020/2021.

- Increasing the small asset depreciation threshold from $500 to $1,000 — and to $5,000 for the 2020/21 tax year.

- Allowing depreciation on commercial and industrial buildings from 2020/2021.

- Removing the hours test from the In-Work Tax Credit (IWTC) from 1 July 2020.

More information on the business cash flow and tax measures can be found from Inland Revenue.

WIDER $12.1 BILLION PACKAGE:

There are further parts to the wider $12.1 billion package that you may be interested in, including income support and further investment in the health response.

More information on the wider package can be found from the Treasury.

Business Finance Support Guarantee Scheme

Please note: Businesses can now start applying to their banks for loans under the Business Finance Guarantee Scheme set up to support the New Zealand economy during the COVID-19 pandemic.

The Government has launched a Business Finance Guarantee Scheme for small and medium-sized businesses, to protect jobs and support the economy. The Crown, in partnership with participating approved banks, will support targeted new loans (including increases to existing limits) to eligible businesses, as a response to difficulties caused by COVID-19.

Under the scheme, businesses with annual revenue between $250,000 and $80 million can apply to their banks for loans up to $500,000, for up to three years. The scheme will offer a total of $6.25 billion in loans to New Zealand businesses.

The Government is guaranteeing 80% of the risk, while the banks are covering the remaining 20%. A normal lending process will be followed by the banks, which will make the lending decisions. Further details can be found on the banks’ websites.

CLICK HERE for more information about the Business Finance Support Guarantee Scheme.

Related Articles:

- BEEHIVE | 01/04/2020 | Business Finance Guarantee – applications open

- BEEHIVE | 25/03/2020 | Working together to protect businesses and workers

- BEEHIVE | 24/03/2020 | Mortgage holiday and business finance support schemes to cushion COVID impacts

Mortgage Holiday Scheme

The package will include a 6 month principal and interest payment holiday for mortgage holders and small to medium sized businesses whose incomes have been affected by the economic disruption from COVID-19.

Related Article:

- BEEHIVE | 24/03/2020 | Mortgage holiday and business finance support schemes to cushion COVID impacts

Insolvency relief for businesses impacted by COVID-19

The Government will be introducing legislation to make changes to the Companies Act to help businesses facing insolvency due to COVID-19 to remain viable, with the aim of keeping New Zealanders in jobs.

The temporary changes include:

- giving directors of companies facing significant liquidity problems because of COVID-19 a ‘safe harbour’ from insolvency duties under the Companies Act

- enabling businesses affected by COVID-19 to place existing debts into hibernation until they are able to start trading normally again

- allowing the use of electronic signatures where necessary due to COVID-19 restrictions

- giving the Registrar of Companies the power to temporarily extend deadlines imposed on companies, incorporated societies, charitable trusts and other entities under legislation

- giving temporary relief for entities that are unable to comply with requirements in their constitutions or rules because of COVID-19.

Read the Cabinet paper | Read the Cabinet minute | Read: How the measures will work

Business Tax Support

Government announced a further set of tax proposals to help businesses manage the impacts of COVID-19. These include:

- greater flexibility for taxpayers in respect to tax deadlines

- changes to the tax loss continuity rules

- a tax loss carry-back scheme.

TEMPORARY LOSS CARRY-BACK SCHEME

This temporary change should be introduced in a bill in the week beginning 27 April.

Businesses expecting to make a loss in either the 2019/20 year or the 2020/21 year would be able to estimate the loss and use it to offset profits in the past year. In other words, they could carry the loss back one year.

This change means IRD could refund some or all the tax already paid for the year they were in profit. It means firms could cash out all or some of their losses in 2019/20 or 2020/21. Without this change, firms would have to carry forward any loss to a year when they make a profit.

PERMANENT LOSS CARRY BACK SCHEME

The Government proposes a permanent loss carry-back scheme, applying to the 2021/22 and later income years. There will be public consultation about this measure in the second half of 2020.

CHANGES TO THE TAX LOSS CONTINUITY RULES

The Government proposes relaxing the tax loss continuity rules. It intends passing legislation before the end of March 2021, and for it to apply to the 2020/21 and later income years.

Currently, if a company has more than a 51% change in ownership it cannot keep its tax losses.

The introduction of a ‘same or similar business’ test, means a business could carry forward losses. To meet the test, the business must continue in the same or a similar way it did before ownership changed. This test is modelled on Australia’s rules.

Increased Business Support

Government announced a further $25 million in funding for the Regional Business Partner Network (RBPN). Approximately $4 million will go to help strengthen call centres to ensure more people can access the service quickly. Roughly $20 million will be invested in the direct business consultancy services to ensure that a wider range of businesses can get the support they need.

To find out what support is available for your business, visit the Regional Business Partner Network website (external link).

Information for...

BUSINESSES AND ORGANISATIONS

BEEHIVE.GOVT.NZ

latest news from beehive.govt.nz

- 01/07/2020: New fund to help save local events and jobs

- 01/07/2020: New Zealand joins global facility for pre-purchase of COVID-19 Vaccine

- 01/07/2020: Infrastructure investment to create jobs, kick-start COVID rebuild

- 22/06/2020: Keeping work safe and fair during and post COVID-19

- 17/06/2020: Government supports more people into industry job training

- 17/06/2020: Backing businesses to upskill New Zealand

BUSINESS.GOVT.NZ

Latest news AND RESOURCES from Business.govt.nz

COVID-19 Latest news and updates: News and updates from government about COVID-19 and how it may affect your business.

COVID-19 Information for businesses: The government’s central resource for COVID-19 business information with updates about COVID-19 and guidance to help businesses.

- 09/06/2020: Workplace operations at Alert Level 1

- 20/05/2020: Contact tracing with NZ COVID Tracer app

AUCKLAND BUSINESS CHAMBER

latest news AND RESOURCES from AUCKLAND BUSINESS CHAMBER

- 16/06/2020: COVID-19 Wage Subsidy Extension

- 04/06/2020: Trans-Tasman bubble test flight readying for take off

- 04/06/2020: Fair Go for SMEs trying to resolve rent disputes

- 02/06/2020: Move to Level 1 – with Confidence and Certainty

- 28/05/2020: Open the Bloody Border

- 28/05/2020: Businesses struggling to find momentum

INLAND REVENUE

LATEST NEWS AND RESOURCES FROM INLAND REVENUE

- 08/06/2020: COVID-19 novel coronavirus New self-service options for customers facing hardship

- 04/06/2020: Tax changes support economic recovery

- 03/06/2020: COVID-19 – Income Relief Payment

- 15/05/2020: Small Business Cashflow (Loan) Scheme NZBN not verifying

- 29/04/2020: COVID-19 (novel coronavirus) – Income equalisation assistance for farmers, fishers and growers

- 15/04/2020: COVID-19 (novel coronavirus) – Tax changes to support businesses